The Federal Reserve increased the benchmark federal funds rate by a quarter point (.25%) yesterday.

As a result, some may have expected consumer mortgage rates to also rise by 25%.

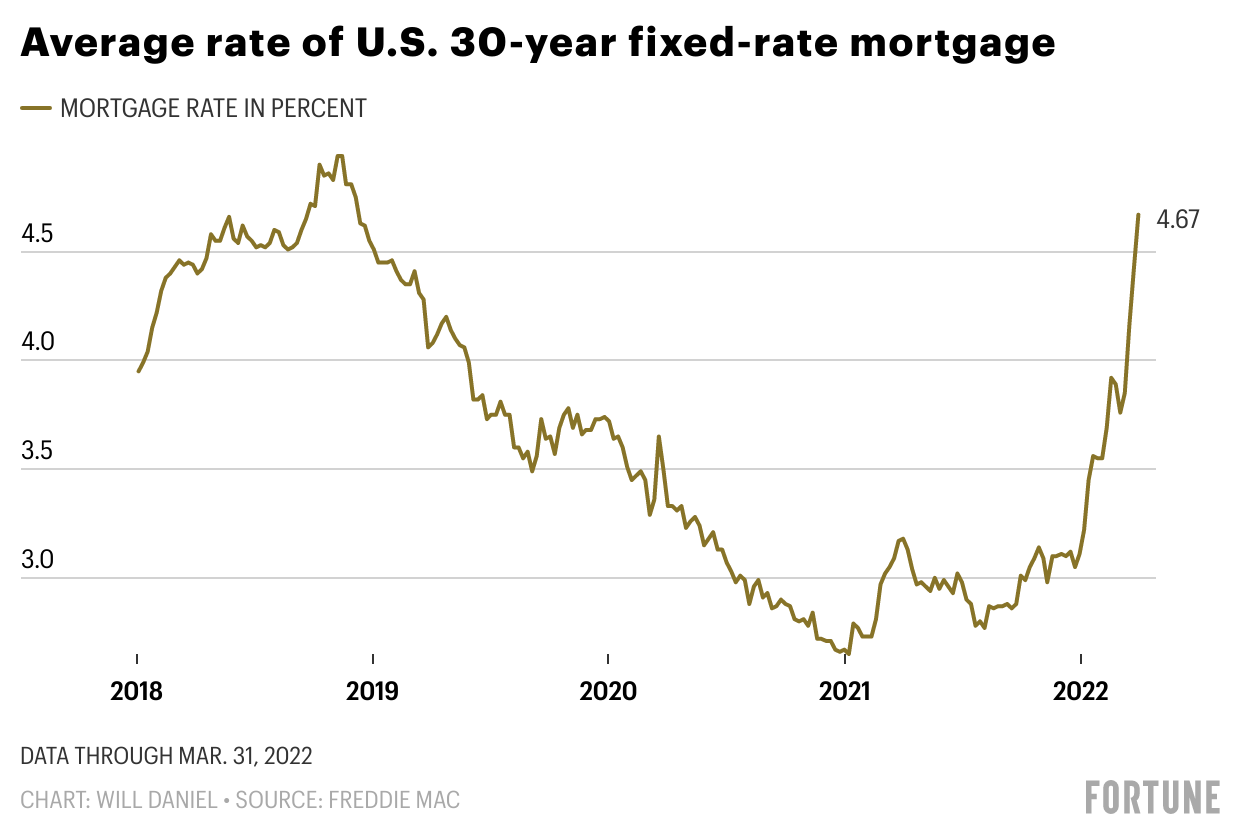

The Fed’s action would cause the 30-year fixed rate, which is currently priced at 6.75%, to increase to 7.00%. However, the opposite happened.

The 30-year fixed rate actually decreased from 6.75% to 6.50%, or about a quarter point.

How come? How can they go in different directions?

Recommended: Does having an overdraft affect getting a mortgage? How a Divorce Can Affect a Reverse Mortgage?

Mortgage rates may decline despite rate increases from the Fed.

As previously mentioned, the Federal Reserve increased the federal funds rate. They have direct control over that interest rate.

And that’s what banks charge one another when using excess reserves overnight. It is not a mortgage interest rate or a consumer interest rate.

However, since there is frequently a trickle-down effect, it does affect consumer lending. In general, banks and lenders follow the Federal Reserve’s lead.

However, the Fed’s announcement of a rate change may completely offset any movement in consumer rates, such as those for home loans.

Why? Because when the Fed releases its Federal Open Market Committee (FOMC) statement, it isn’t just increasing or decreasing rates.

Additionally, it provides background information for any Fed Funds rate increases or decreases. We can infer movements in mortgage rates from this context.

How did yesterday go? Mortgage rates decreased as the Fed raised rates.

The Federal Reserve raised the target fed funds rate to a range of 4-3/4 percent to 5 percent in the FOMC statement from March 22, 2023.

Although it was possible that they could have done nothing, this was largely expected.

However, the general consensus was that they wanted to calm the markets without completely ceasing their rate increases while also avoiding upsetting the markets with a larger increase, such as 0.50%.

There was, however, more to the tale. They discussed both the present situation and the outlook for the future in the FOMC statement.

And since the release on February 1, 2023, their statement has changed. Here are the main changes:

The Committee previously stated that “continuous increases in the target range will be appropriate” in order to achieve a stance of monetary policy that is sufficiently restrictive to bring inflation back to 2 percent over time.

This was taken to mean that a number of rate increases would be required to control inflation, which would probably also result in an increase in consumer interest rates.

After all, additional rate increases would be required to lower inflation to its target of 2% if the outlook called for persistent inflation.

“The Committee anticipates that some additional policy firming may be appropriate to achieve a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time,” they stated in the release from yesterday.

As a result, we changed from “ongoing increases” to “some additional policy firming” that may be appropriate.

That definitely sounds more dovish and softer. One might also contend that they have already reached the maximum increase in the fed funds rate they anticipate, or their terminal rate.

Possible end to the Fed’s rate hikes

The Fed essentially stated that it is finished raising rates. This might result in a 0.25% increase all told.

As a result, long-term mortgage rates let out a sigh of relief.

Why? Because it is anticipated that rates have essentially peaked and may even start to decline later this year.

Although the Fed does not directly control mortgage rates, the direction of rates is influenced by the Fed’s policy choices.

We can anticipate a more accommodating rate policy if they are telling us the job is largely finished.

Additionally, the recent banking crisis may lead to tighter lending standards. Less money is moving around the economy as a result, which has a deflationary effect as well.

To cut a long story short, this releases the Fed from pressure to raise its own rate.

Simply watch out for tighter lending requirements.

One warning: If the banking industry faces more pressure, consumers may not have access to credit.

It might be more challenging to obtain a home loan if banks and mortgage lenders are less willing to lend.

Also, their pricing may be conservative. This suggests that the gap between the yield on the 10-year Treasury and the rate on a 30-year mortgage could widen even more.

Mortgage rates may therefore continue to be higher than they should be, even if the yield on the 10-year bond drastically drops.

Additionally, individuals with lower FICO scores and/or higher DTI ratios may experience greater difficulty obtaining a low-cost mortgage or any type of mortgage.

In the interim, you might be able to lock in a mortgage rate that is a little bit lower than it was a week ago. Just be aware of daily volatility, which is comparable to the stock market.

But if the pattern holds, we might observe significant changes in interest rates later in 2023 and possibly into 2024.

It will be interesting to see if mortgage rates in the 4% range return.

Leave a Reply