When you’re looking to buy a home, one of the first things you need to consider is whether to take out a mortgage. There are pros and cons to taking out a mortgage, and it’s important to weigh them both before making a decision.

On the plus side, a mortgage can be a good way to finance a home purchase. If you don’t have the cash on hand to buy a home outright, a mortgage can help you get into the home of your dreams. Additionally, a mortgage can be a good way to build equity in your home. As you make your monthly payments, you’ll slowly but surely be building up equity in your home.

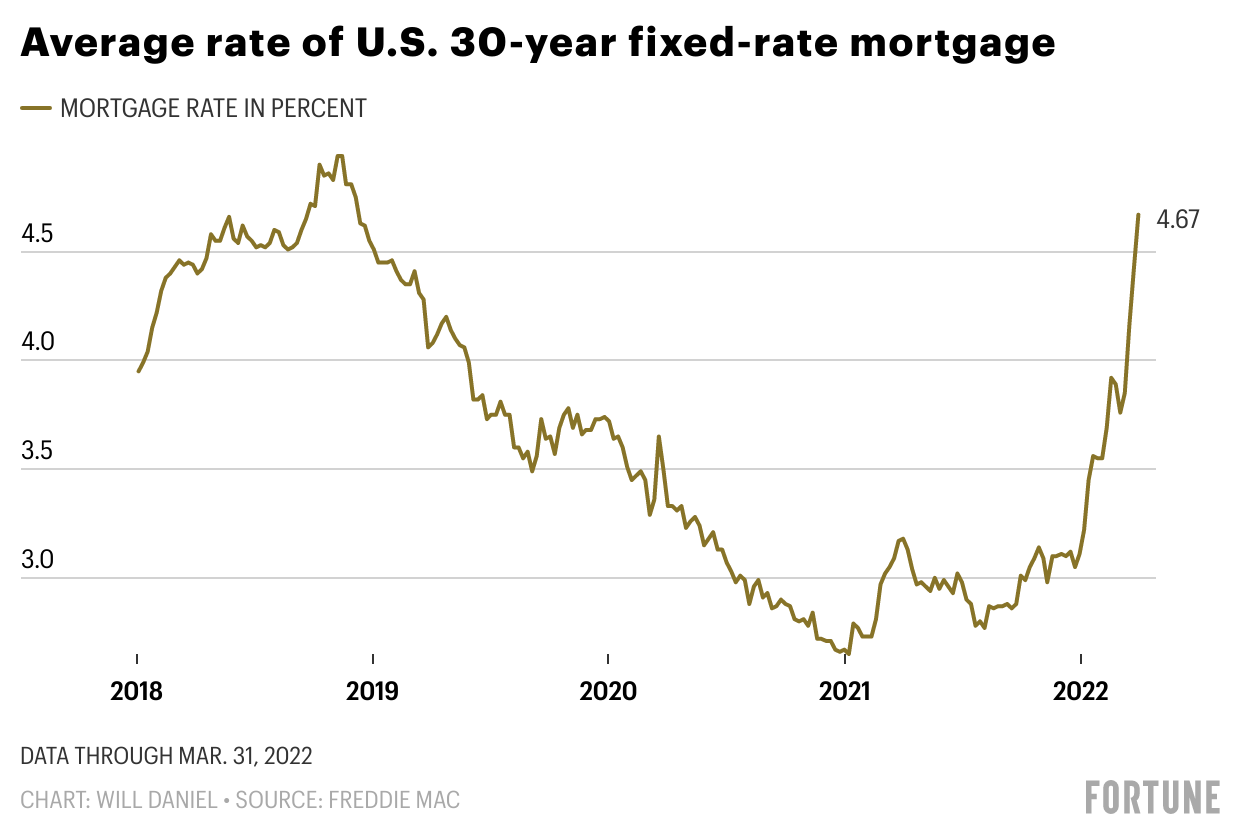

Recommended: Does having an overdraft affect getting a mortgage? Understanding the Relationship Between Mortgage Rates and Fed Rate Hikes On the downside, a mortgage can be a risky investment. If you take out a mortgage and then find yourself unable to make your monthly payments, you could end up losing your home. Additionally, a mortgage can be a pricey investment, as you’ll likely have to pay interest on your loan.

Ultimately, whether or not a mortgage is a good idea for you will come down to your circumstances. If you feel confident that you can make your monthly payments and are comfortable with the risks, a mortgage can be a great way to finance your home purchase. However, if you’re not sure you can make the payments or are uncomfortable with the risks, it might be best to steer clear of a mortgage and look for alternative financing options.

When it comes to bonuses and mortgages, there are a few things to keep in mind. For starters, bonuses are often treated as supplemental income, which means that they may not be considered when your mortgage application is being processed.

There are a few reasons for this. For one, bonuses are often irregular, which makes it difficult to predict how much money you’ll have coming in on a month-to-month basis. This can make it difficult for lenders to properly assess your ability to make your monthly mortgage payments.

Additionally, bonuses are often paid out in lump sums, which can make it difficult to budget and save for a down payment or other upfront costs associated with buying a home.

That said, some lenders will take bonuses into account when considering your mortgage application. If you have a history of consistent bonus payments, this could be viewed as evidence of your ability to manage your finances and make regular mortgage payments.

If you’re hoping to have your bonus considered as part of your mortgage application, it’s important to be upfront about it with your lender. There may be some additional documentation required, such as proof of bonus payments for the past few years.

At the end of the day, whether or not your bonus is taken into account for mortgage purposes will depend on the lender you’re working with. It’s always best to be upfront and honest about your income and financial situation so that you can find a lender who’s willing to work with you.

3) What to do if your bonus is about to be paid.

A bonus is a financial reward given to an employee for good performance. While bonuses are typically given in the form of cash, they may also be given as stock options, merchandise, or other forms of compensation. If you’re considering applying for a mortgage, you may be wondering if your bonus will be counted as part of your salary. The answer to this question depends on the lender. Some lenders will count a bonus as part of your salary, while others will not. If you’re not sure whether or not your bonus will be counted, it’s best to speak to a mortgage specialist to find out.

1) Does a bonus count as salary for a mortgage

A bonus is a great way to reward yourself for a job well done. But what should you do if your bonus is about to be paid and you’re not sure what to do with it?

Here are three things to consider if your bonus is about to be paid:

1. Save it.

If you’re not sure what to do with your bonus, a safe option is to simply save it. You can put it into a savings account or an investment account, and let it grow over time. This way, you’ll have the money available if you need it in the future, but you won’t be tempted to spend it on something you don’t really

There are a few key things that you can do to maximize your chances of being approved for a mortgage. Firstly, make sure that you are on the electoral roll and have a good credit score. You can improve your credit score by paying your bills on time and not opening too many new lines of credit.

Secondly, try to avoid any significant changes in your employment situation. Lenders like to see stability, so if you can, try to stay in your current job and at the same salary level.

Thirdly, make a large down payment. The larger the down payment, the lower the risk for the lender and the more likely you are to be approved for a mortgage.

Fourthly, consider using a mortgage broker. A mortgage broker can help you find the best mortgage rates and terms for your situation.

Lastly, remember that the process takes time. Don’t get discouraged if you are not approved for a mortgage right away. Keep working on your credit score and employment situation, and try again in a few months.

5) The pros and cons of taking out a mortgage.

need.

2. Use it to pay off debt.

If you have any high-interest debt, such as credit card debt, using your bonus to pay it off can be a smart move. This can save you a lot of money in interest charges, and it can help you get out of debt more quickly.

3. Use it to buy something you’ve been wanting.

If you’ve been wanting to buy a new car or take a vacation, using your bonus to do so can be a great way to enjoy your hard-earned money. Just be sure to not overspend and to keep your financial goals in mind.

No matter what you do with your bonus, be sure to think carefully about it before making any decisions. A bonus can be a great opportunity to improve your financial situation, but it can also be a way to set yourself back if you’re not careful.

4) How to maximize your chances of getting a mortgage.

?

When you’re applying for a mortgage, lenders will look at your income and debts to determine how much you can afford to borrow. Your income includes your salary, any bonuses or commissions you receive, and other sources of income such as alimony or child support.

If you receive a bonus or commission, you may be able to use it to qualify for a mortgage. Lenders typically require that you have a certain amount of “guaranteed income” to qualify for a loan. This means that if your bonus or commission is a large part of your income, you may not qualify for a loan unless you have a history of receiving similar payments.

If you’re self-employed, your income may be more difficult to verify. Lenders will typically require additional documentation such as tax returns or profit and loss statements.

If you’re receiving income from sources other than employment, such as child support or alimony, you’ll need to provide documentation of these payments. Lenders may also require that these payments be made through a third party such as an employer or the government.

Income from investments can also be used to qualify for a mortgage. Lenders will typically require documentation of your investment income, such as bank statements or investment account statements.

Bottom line: If you’re using income from bonuses, commissions, or other sources to qualify for a mortgage, be prepared to provide documentation of these payments to your lender.